| Income Tax (Amendment) Bill |

Bill No. 14/2013

| Read the first time on 16th September 2013. |

| An Act to amend the Income Tax Act (Chapter 134 of the 2008 Revised Edition) and to make a consequential amendment to the Economic Expansion Incentives (Relief from Income Tax) Act (Chapter 86 of the 2005 Revised Edition). |

| Be it enacted by the President with the advice and consent of the Parliament of Singapore, as follows: |

| Short title and commencement |

| Amendment of section 2 |

2. Section 2(1) of the Income Tax Act (referred to in this Act as the principal Act) is amended by inserting, immediately after the definition of “incapacitated person”, the following definition:

|

| Amendment of section 6 |

3. Section 6 of the principal Act is amended —

|

| Amendment of section 10 |

4. Section 10 of the principal Act is amended —

|

| Amendment of section 10C |

5. Section 10C of the principal Act is amended —

|

| Amendment of section 10F |

6. Section 10F of the principal Act is amended —

|

| Amendment of section 13 |

7. Section 13 of the principal Act is amended —

|

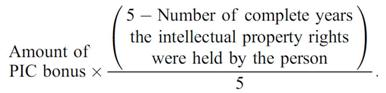

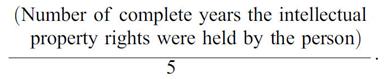

| Repeal and re-enactment of section 13B |

8. Section 13B of the principal Act is repealed and the following section substituted therefor:

|

| Amendment of section 13J |

9. Section 13J of the principal Act is amended —

|

| Amendment of section 13L |

10. Section 13L of the principal Act is amended —

|

| Amendment of section 13M |

11. Section 13M of the principal Act is amended by inserting, immediately after subsection (5), the following subsection:

|

| Amendment of section 13P |

12. Section 13P of the principal Act is amended —

|

| Amendment of section 14 |

13.—(1) Section 14 of the principal Act is amended —

|

| Repeal of section 14J |

| 14. Section 14J of the principal Act is repealed. |

| Amendment of section 14Q |

| 15. Section 14Q(7) of the principal Act is amended by deleting “$15,000” in paragraph (d)(ii) and substituting “$150,000”. |

| New section 14V |

16. The principal Act is amended by inserting, immediately after section 14U, the following section:

|

| New section 14W |

17. The principal Act is amended by inserting, immediately after section 14V, the following section:

|

| Amendment of section 15 |

18.—(1) Section 15 of the principal Act is amended —

|

| Amendment of section 19 |

19. Section 19(4) of the principal Act is amended by deleting paragraph (b) and substituting the following paragraph:

|

| Amendment of section 21 |

20. Section 21 of the principal Act is amended by deleting subsection (5) and substituting the following subsection:

|

| Amendment of section 26 |

21.—(1) Section 26 of the principal Act is amended —

|

| Amendment of section 34C |

| 22. Section 34C(30) of the principal Act is amended by inserting, immediately after the words “amalgamated company” in paragraph (e), the words “and an amalgamating company”. |

| Amendment of section 37I |

23.—(1) Section 37I of the principal Act is amended —

|

| New sections 37IA and 37IB |

24. The principal Act is amended by inserting, immediately after section 37I, the following sections:

|

| Amendment of section 37J |

25. Section 37J of the principal Act is amended —

|

| Amendment of section 37M |

26. Section 37M(1) of the principal Act is amended by deleting paragraph (b) and substituting the following paragraph:

|

| Amendment of section 43 |

27. Section 43 of the principal Act is amended —

|

| Amendment of section 43N |

| 28. Section 43N of the principal Act is amended by deleting the words “31st December 2013” in subsections (1)(aa)(ii), (ab) and (ac), (2)(a), (b)(ii), (c) and (d) and (3)(b) and substituting in each case the words “31st December 2018”. |

| Repeal of section 43O |

| 29. Section 43O of the principal Act is repealed. |

| Amendment of section 43ZC |

30. Section 43ZC of the principal Act is amended —

|

| Amendment of section 45 |

| 31. Section 45(9) of the principal Act is amended by deleting the words “31st December 2013” in paragraph (a) and substituting the words “31st December 2018”. |

| Amendment of section 45A |

| 32. Section 45A of the principal Act is amended by deleting the words “31st December 2013” in subsections (2)(b), (2A) and (2B)(a) and substituting in each case the words “31st December 2018”. |

| Amendment of section 65B |

33. Section 65B of the principal Act is amended —

|

| Repeal and re-enactment of section 65C and new sections 65D and 65E |

34. Section 65C of the principal Act is repealed and the following sections substituted therefor:

|

| New section 92D |

35. The principal Act is amended by inserting, immediately after section 92C, the following section:

|

| Amendment of section 93A |

36. Section 93A of the principal Act is amended —

|

| Amendment of section 94 |

| 37. Section 94 of the principal Act is amended by deleting subsection (5). |

| Amendment of section 95 |

38. Section 95 of the principal Act is amended —

|

| Amendment of section 96 |

39. Section 96 of the principal Act is amended —

|

| Amendment of section 96A |

40. Section 96A of the principal Act is amended —

|

| Amendment of section 105A |

41. Section 105A of the principal Act is amended —

|

| Amendment of section 105B |

| 42. Section 105B of the principal Act is amended by deleting the words “prescribed under section 105C” in paragraphs (a) and (b). |

| Repeal of section 105C |

| 43. Section 105C of the principal Act is repealed. |

| Amendment of section 105D |

44. Section 105D of the principal Act is amended by inserting, immediately after subsection (3), the following subsection:

|

| Amendment of section 105E |

45. Section 105E of the principal Act is amended —

|

| Amendment of section 105F |

46. Section 105F of the principal Act is amended by deleting subsection (1) and substituting the following subsection:

|

| New section 105GA |

47. The principal Act is amended by inserting, immediately after section 105G, the following section:

|

| Repeal and re-enactment of Part XXB |

48. Part XXB of the principal Act is repealed and the following Part substituted therefor:

|

| Miscellaneous amendments arising from abolition of imputation system |

49.—(1) The provisions of the principal Act specified in the first column of the Schedule are amended in the manner set out in the second column of that Schedule.

|

| Miscellaneous amendments |

50. The principal Act is amended by deleting “43O,” in the following sections:

|

| Remission of tax for year of assessment 2013 |

51.—(1) There shall be remitted the tax payable for the year of assessment 2013 by an individual resident in Singapore an amount equal to —

|

| Savings provision |

52.—(1) Notwithstanding section 27(a), section 43(5) of the principal Act in force immediately before the date the Income Tax (Amendment) Act 2013 is published in the Gazette shall apply to any payment made before that date of income from a profession or vocation to an individual or foreign firm to which section 43(4) of the principal Act applies.

|

| Consequential amendment to Economic Expansion Incentives (Relief from Income Tax) Act |

| 53. Section 66(1) of the Economic Expansion Incentives (Relief from Income Tax) Act (Cap. 86) is amended by deleting “43O,” in the definition of “concessionary income”. |